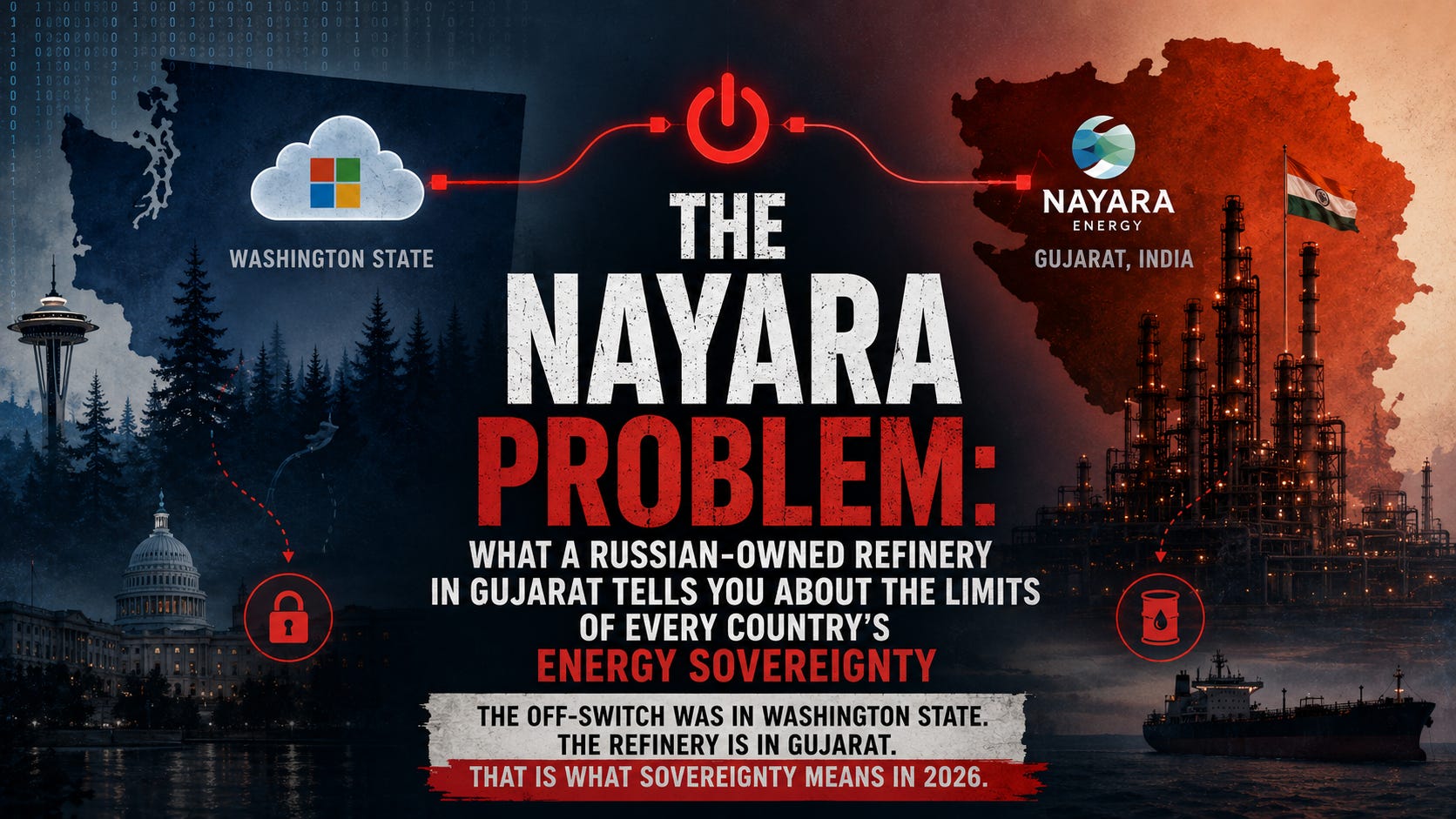

The Nayara Problem: What a Russian-Owned Refinery in Gujarat Tells You About the Limits of Every Country’s Energy Sovereignty

The off-switch was in Washington state. The refinery is in Gujarat. That is what sovereignty means in 2026.

One refinery. Four unsolvable problems. The moment when Russia’s largest energy investment in India became a liability for everyone who owns it, everyone who sanctions it, and everyone who depends on it.

On July 22, 2025, Microsoft suspended Outlook, Teams, and cloud data access to Nayara Energy India’s second-largest private refinery, processing 8% of the country’s crude throughput without prior notice, without legal obligation under US or Indian law, and without a plan for restoring 7 years of operational data stored on its servers.

Nayara’s response: sue Microsoft in the Delhi High Court, switch email to Rediff.com, and file an emergency injunction to recover access to its own data. Microsoft restored services eight days later, hours before the hearing, and said nothing further about what it would do next time.

The Indian Finance Ministry’s response, published in April 2026: draft a domestic blocking statute modelled on a 1996 EU law that prevents Indian-registered companies from complying with foreign sanctions imposed on Indian soil effectively making it illegal for Microsoft to do again what it just did.

A US technology company enforcing a European sanction on an Indian refinery, in a jurisdiction where neither the US nor European sanction has legal force, is not a corporate compliance story. It is the most precise demonstration available of what energy sovereignty actually means in 2026: not the right to produce your own oil, but the right to run your own refinery without a foreign company being able to shut it down from a cloud server in Redmond, Washington.

🎯 What this article gives you

By the end of this, you’ll know:

→ The Nayara ownership structure in full and why every party that owns a piece of it is now trying to exit without a buyer capable of paying

→ The four unsolvable problems: the EU sanction, the Microsoft precedent, the Rosneft exit that cannot close, and the Hormuz war that made the feedstock politically toxic

→ The digital sovereignty dimension: why the Microsoft incident exposed a chokepoint in India’s critical infrastructure that nobody had mapped before it was exploited

→ The three historical cases where foreign energy investment in a country became a geopolitical liability BP in Russia, Aramco’s nationalization, and Shell’s Nigeria and what each one tells you about the exit options available to Nayara’s owners

→ The five parties who need a resolution and the specific reason each one cannot achieve it cleanly

→ Why the Nayara problem is not unique to India and the pattern it names for every country that accepted foreign direct investment in strategic energy infrastructure during a period of geopolitical alignment

📍 Start here: the refinery that nobody can afford to let fail

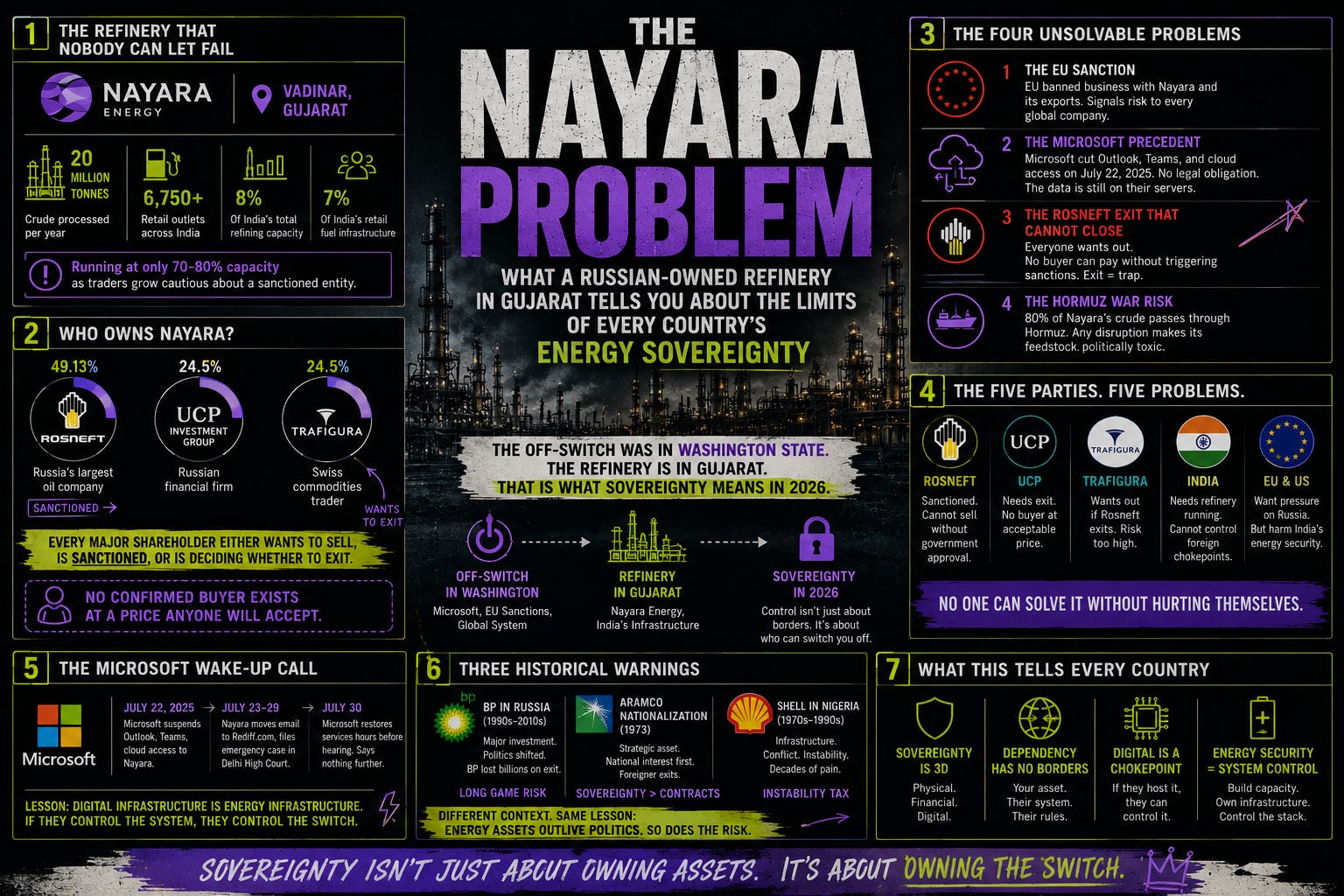

Vadinar, Gujarat. The Nayara Energy refinery sits at the edge of the Gulf of Kutch, a few kilometres from Reliance’s Jamnagar complex the largest refining site in the world.

Nayara’s refinery processes 20 million tonnes of crude per year. It supplies petroleum products to 6,750 retail outlets across India the largest private fuel retail network in the country. It accounts for approximately 8% of India’s total refining capacity and 7% of its retail fuel infrastructure.

It is also 49.13% owned by Rosneft, Russia’s largest oil company, which is under sanctions from the United States, the European Union, and the United Kingdom. The other major shareholders are UCP Investment Group, a Russian financial firm, holding 24.5%, and Trafigura, a Swiss commodities trader, holding 24.5%.

Every major shareholder of India’s second-largest private refinery either wants to sell, is sanctioned, or is deciding whether to exit if a sale happens. No confirmed buyer exists at a price anyone will accept. And the refinery is currently running at 70 to 80% capacity because traders are growing cautious about dealing with a sanctioned entity.

This is the Nayara Problem. It is not primarily an energy story. It is a sovereignty story. And it has no clean resolution available to any of the five parties who need one.

⚖️ The four unsolvable problems why every exit is blocked

Problem 1: The EU sanction that India did not ask for and cannot reverse.

On July 18, 2025, as part of its 18th sanctions package targeting Russian oil revenues, the EU designated Nayara Energy’s Vadinar refinery as subject to sanctions, citing its status as the “biggest Rosneft refinery in India.”

The EU sanction does three specific things. It prohibits EU-registered companies from doing business with Nayara. It prevents Nayara from exporting refined petroleum products petrol, diesel, jet fuel to EU member states. And it signals to every multinational corporation with EU operations that servicing Nayara carries compliance risk, regardless of what Indian or US law says.

Nayara’s statement captured the precise contradiction: “While many European countries continue to import Russian energy through various sources, they take a high moral ground by chastising and sanctioning an Indian asset for processing Russian crude largely used by its domestic population of 1.4 billion Indians and businesses.”

The EU does not sanction Rosneft’s investments in Germany, Austria, or Hungary EU member states that continued importing Russian oil for years after the Ukraine invasion through pipeline infrastructure the sanctions framework exempted. It sanctioned a refinery in India. The selectivity of this application is the source of India’s indignation and the basis of its proposed legislative response.

Problem 2: The Microsoft incident and what it proved about digital infrastructure dependency.

On July 22, 2025 four days after the EU designation Microsoft suspended all cloud services to Nayara: Outlook, Teams, and cloud storage. The suspension was done without prior notice, without consultation, and without any legal requirement under either US or Indian law.

Neither Indian law nor US regulations required Microsoft to enforce these sanctions. The company acted on its own interpretation of EU directives, sidelining Indian sovereignty and legal frameworks.

Nayara was left without access to its own data. Its workforce could not email internally. Its operations team could not access documents stored on Microsoft servers. Its compliance records required for Indian regulatory filings were inaccessible. The company turned to Rediff.com, a Mumbai-based provider, for basic email functions, unable to access the historical correspondence that remained on Microsoft’s servers.

The Delhi High Court filed an emergency petition. Microsoft restored services eight days later, hours before the scheduled hearing on July 30 acknowledging, through the timing of the restoration, that its action was not legally defensible.

The precedent this set is more significant than the incident. A US corporation, acting on its interpretation of a European sanction, in a jurisdiction where neither sanction has legal authority, was able to paralyze critical operations of a facility processing 8% of India’s crude throughput. It did so for eight days. It could do so again.

The Indian Finance Ministry’s response proposing a domestic blocking statute modelled on the EU’s own 1996 law that shields European companies from extraterritorial third-country sanctions is the first legislative response to the principle that Western sanctions architecture can be enforced by private technology companies on Indian soil without any legal basis in Indian law. The ministry also proposed requiring critical sectors to use domestically built sovereign cloud infrastructure. India’s cloud services market has reached more than $27 billion. Microsoft and AWS account for the majority of that market. The Finance Ministry proposal, as of April 2026, has not yet been enacted.

Problem 3: The Rosneft exit that cannot close.

Rosneft acquired Essar Oil later renamed Nayara Energy in 2017 as part of a $12.9 billion transaction. It was the largest foreign direct investment in India’s refining sector. It was completed at a time when US-Russia sanctions existed but were not yet sufficiently comprehensive to prevent normal business operations.

By 2024, Western sanctions had made it effectively impossible for Rosneft to repatriate earnings from its Indian operations. The refinery was generating cash. Rosneft could not move that cash out of India in any usable form. It decided to exit.

The stake was offered to Reliance Industries, the Adani Group, Saudi Aramco, and a state-owned ONGC-IOC consortium.

Adani Group declined. Its partnership agreement with Total Energies includes a commitment to limit future fossil fuel investments to natural gas, which a refinery acquisition would violate. Beyond that contractual constraint, Adani’s strategic positioning treats oil refining as a sunset business incompatible with its renewable energy identity.

The ONGC-IOC consortium valued the marketing network at no more than Rs 3 to 3.5 crore per outlet, giving a total marketing network valuation of approximately $2.5 to 3 billion a fraction of Rosneft’s initial $20 billion ask.

Saudi Aramco has long sought a downstream presence in India and remains interested. But Aramco also considers the valuation steep, and its relationship with the Indian government is complicated by a stalled maharefinery project in Maharashtra that has produced no progress in five years.

Reliance Industries remains the most strategically logical buyer. Nayara’s Vadinar refinery sits adjacent to Reliance’s Jamnagar complex. A combined operation would exceed IOC’s 80.8 million tonnes per year to make Reliance India’s largest refiner. The 6,750 Nayara petrol pumps would give Reliance, which currently operates only 1,972 of India’s 97,366 fuel stations, a meaningful position in fuel retail. Reliance’s internal valuation of the retail network is estimated at Rs 7 crore per outlet, and it sees significant petrochemical synergies worth a further $5 billion.

Rosneft has reduced its asking price from $20 billion to approximately $17 billion. Reliance still considers this too high.

The EU sanction of July 2025 has made the valuation problem worse, not better. A buyer of Nayara must now account for the EU export restriction, the ongoing compliance risk from multinational service providers, the reputational cost of acquiring a sanctioned entity, and the operational uncertainty of a refinery running at 70 to 80% capacity because traders are cautious about dealing with it. The price Rosneft wants reflects the asset before the sanction. The price any buyer will offer reflects the asset after it.

Problem 4: The Hormuz war made the feedstock politically toxic at the worst moment.

Nayara processes Russian crude predominantly. Its refinery configuration is optimized for Russian Urals grade oil. The Hormuz war, which began on February 28, 2026, simultaneously increased global demand for Russian crude as an alternative to blocked Gulf supply and increased the political pressure on India to reduce Russian crude purchases as part of the US trade deal framework signed on February 2.

The Hormuz war made Russian crude more valuable globally. It also made India’s dependence on Russian crude more politically visible to Washington. Nayara which processes Russian crude and is majority-owned by a sanctioned Russian entity became the most politically sensitive refinery in India at the moment when India’s energy alignment was most actively contested.

The refinery India cannot afford to shut down is the refinery whose ownership, feedstock, and geopolitical association have become the most complicated in the country.

💬 “Nayara is the point where the Russia-Ukraine war, the Hormuz crisis, the US-India trade deal, the EU sanctions architecture, and India’s cloud infrastructure dependency all intersect at a single industrial facility in Gujarat. There is no solution that satisfies all five simultaneously. That is not a policy failure. That is the definition of a geopolitical trap.”

Case 1: BP in Russia. The investment that became a hostage.

British Petroleum’s journey into Russian energy began in 1997 with a minority stake in Sidanco, a Russian oil company. By 2003, BP had formed TNK-BP a 50-50 joint venture with Russian oligarchs Mikhail Fridman, Leonard Blavatnik, and their partners, combining BP’s technology and capital with Russia’s largest oil assets.

TNK-BP was, by the mid-2000s, one of Russia’s largest oil producers. It contributed approximately a quarter of BP’s global production and a third of its profits. BP was not merely invested in Russia. Russia was central to BP’s global strategy.

In 2012, Rosneft acquired TNK-BP in a $55 billion transaction, converting BP’s stake to a 19.75% shareholding in Rosneft itself making BP the largest foreign shareholder in a Russian state company.

When Russia invaded Ukraine in February 2022, BP’s board voted to exit the Rosneft stake. The announced write-down was approximately $25 billion. The actual exit took three years of negotiations, legal proceedings, and political pressure. As of 2025, BP had still not extracted meaningful cash value from the position. The Russian government placed restrictions on dividend payments and asset transfers that prevented a clean exit.

BP’s Russian investment generated extraordinary returns for 25 years and then generated a $25 billion write-down in 48 hours. The investment had become a hostage an asset that could not be exited because the regulatory environment in which it was held had changed beyond recognition.

The structural lesson for Nayara:

BP’s Rosneft stake is the precedent. An energy asset held in a geopolitically aligned relationship generates returns as long as the alignment holds. When the alignment breaks through war, sanctions, or political reorientation the exit becomes the most expensive part of the investment. Rosneft paid $12.9 billion for Nayara in 2017. It cannot extract the value it paid for because the regulatory environment in which it made the investment no longer exists.

The difference between the BP case and the Nayara case: BP was the Western party in a Russian asset. Rosneft is the Russian party in an Indian asset. In the BP case, the Russian government controlled the exit. In the Nayara case, it is the Western sanctions architecture and a US technology company’s compliance interpretation of that architecture that controls the operational environment of the asset.

💬 “BP’s Rosneft stake taught the energy industry that a foreign asset held under geopolitical alignment generates returns as long as the alignment holds. When it breaks, the write-down arrives in 48 hours. Rosneft paid $12.9 billion for Nayara in 2017. The alignment has broken. The write-down is being negotiated in real time.”

Case 2: Aramco’s nationalization, 1973-1980. When sovereignty reclaimed the asset.

The Arabian American Oil Company Aramco was created in 1933 by Standard Oil of California, which had obtained a 60-year concession from Saudi Arabia to explore and extract oil. By 1948, Standard Oil, Texaco, Exxon, and Mobil had all taken stakes. By 1972, Aramco controlled the world’s largest oil reserves, operated by US companies, with Saudi Arabia receiving royalties as a landlord.

In 1973, Saudi Arabia acquired a 25% stake in Aramco as part of a negotiated nationalization process. The stake rose to 60% in 1974. By 1980, Saudi Arabia had acquired 100% of Aramco, renaming it Saudi Aramco, and began operating the world’s largest oil company as a sovereign instrument.

The US companies received compensation. They retained offtake agreements. They maintained technical roles for years. The transition was structured to be commercially manageable for all parties.

What made this nationalization structurally different from Nayara:

Saudi Arabia was the host country, the sovereign, and the party with the leverage. It set the terms of the transition. The US companies had no choice but to negotiate because the alternative losing the asset entirely without compensation was worse than accepting the nationalization terms.

In the Nayara case, the structure is inverted. The host country India has not nationalized the asset. It does not want to. India has no interest in acquiring a Russian-owned refinery at a valuation dispute and inheriting the associated geopolitical complications. India wants the Rosneft exit to happen through a commercial transaction that produces an Indian owner, at a price Rosneft will accept, without triggering further sanctions exposure or requiring Indian government intervention.

That transaction has not happened in two years of active effort. The Aramco nationalization happened because the sovereign had both the leverage and the strategic interest. India has the leverage but not the strategic interest in acquiring the complication.

💬 “The Aramco nationalization took seven years and produced the world’s most valuable company. India could nationalize Nayara tomorrow. It won’t. Because the thing that makes nationalization work is wanting to own what you’re nationalizing. India does not want to own a Russian-associated liability during the most contested energy alignment decision of its post-independence history.”

Case 3: Shell in Nigeria. The asset you cannot exit and cannot operate cleanly.

Shell has operated in Nigeria’s Niger Delta since 1958, first through the Shell-BP joint venture and then as the operator of SPDC Shell Petroleum Development Company of Nigeria a joint venture with the Nigerian National Petroleum Corporation.

Shell’s Nigeria operations have generated extraordinary oil revenues and documented environmental disasters simultaneously for 65 years. Oil spills from Shell infrastructure both from equipment failure and from deliberate sabotage by local communities protesting the environmental conditions have contaminated agricultural land and fishing grounds across the Niger Delta.

Shell repeatedly attempted to exit Nigeria. Each attempt was blocked by the Nigerian government, which did not want to lose Shell’s technical capacity, or by financial complications, or by the inability to find a buyer willing to accept the environmental liability that comes with the asset.

In 2023, Shell announced a definitive agreement to sell its SPDC stake for $2.4 billion to the Renaissance consortium. The transaction took two years to close due to Nigerian regulatory requirements, disputes over environmental remediation liability, and financing complications for the buyers.

The structural lesson:

The asset Shell could not cleanly operate and could not cleanly exit was held for 65 years between the first operational difficulty and the sale closing. The host country’s regulatory requirements, the environmental liability attached to the asset, and the absence of a qualified buyer at an acceptable price combined to make Shell’s position permanently uncomfortable and permanently inescapable.

Nayara’s timeline is shorter eight years from acquisition to exit attempt but the structural dynamic is identical. Rosneft holds an asset it cannot operate cleanly (due to sanctions), cannot exit cleanly (due to valuation disagreement and buyer complications), and cannot simply abandon (due to the $12.9 billion original investment and the reputational cost of an uncompensated exit).

🌍 What the Nayara problem means for every country that accepted foreign energy FDI

Every country that accepted foreign direct investment in strategic energy infrastructure during a period of geopolitical alignment has a version of the Nayara problem waiting to be activated.

The specific trigger is geopolitical realignment. When the political relationship between the investing country and the host country changes through war, sanctions, trade disputes, or alliance shifts the foreign-owned infrastructure becomes a liability simultaneously for the investor (who cannot extract returns), the host country (which cannot control the strategic asset), and the workers and communities dependent on the facility.

The pattern has three phases:

Phase 1 — The alignment period: foreign investment flows in, infrastructure is built or acquired, returns are generated, the relationship is described as a strategic partnership.

Phase 2 — The disruption: geopolitical realignment occurs, sanctions are imposed, the investment’s financial flows are blocked, the regulatory environment in which the investment was made no longer exists.

Phase 3 — The trap: the asset cannot be operated cleanly, cannot be exited cleanly, and cannot be nationalized without political cost. All parties are stuck. The facility continues operating at reduced capacity while the resolution is negotiated, indefinitely.

Nayara is in Phase 3.

The digital sovereignty dimension - the layer nobody saw coming

The Microsoft incident added a new dimension to Phase 3 that no previous case had encountered. In Shell’s Nigeria, BP’s Russia, or Aramco’s Saudi Arabia, the geopolitical trap was physical and financial. A foreign company owned a physical asset in a country where the political environment had changed. The resolution involved physical negotiations about physical assets.

In Nayara’s case, a US technology company was able to paralyze the operations of a physical refinery by suspending access to a cloud service. The physical refinery is in Gujarat. The off-switch was in Washington state. Neither the EU sanction that prompted the action nor the US law under which Microsoft operates required it to flip that switch.

The Indian Finance Ministry is now proposing a blocking statute and a sovereign cloud policy. Both are correct responses to a vulnerability that was not visible until it was exploited. Both are 12 to 18 months from implementation at minimum.

In the interim, every Indian company that depends on foreign cloud infrastructure for operational continuity faces the same vulnerability that Nayara faced on July 22, 2025. The cloud infrastructure of a $3.7 trillion economy runs primarily on servers owned by two US companies. Those servers can be made inaccessible to any Indian entity that falls within the compliance interpretation of any foreign sanction without legal authority in India, without prior notice, and without obligation to restore services.

This is not a technology story. It is a sovereignty story told through a cloud service suspension.

The five parties who need a resolution and why each one cannot achieve it

Rosneft: Needs to sell, cannot repatriate earnings, wants $17 billion, has no confirmed buyer at that price. Has visited India three times in the past year seeking buyers. Has reduced its ask from $20 billion. Cannot reduce further without acknowledging the EU sanction has materially impaired the asset value.

India’s government: Cannot nationalize without inheriting the geopolitical liability. Cannot force a sale without triggering WTO arbitration. Cannot ignore the operational implications of a sanctioned refinery processing 8% of the country’s crude throughput. Is simultaneously negotiating an energy alignment framework with Washington that increases the political cost of appearing to protect a Russian asset.

The EU: Sanctioned the asset but cannot enforce the sanction within Indian jurisdiction. Depends on India’s cooperation for its own trade and strategic interests, including the India-EU FTA concluded January 27, 2026. Has no mechanism to compel the resolution it wants Rosneft’s exit without Indian cooperation it has undermined by sanctioning Indian soil.

Reliance Industries: The most logical buyer, currently in preliminary talks, finds the $17 billion ask too high for an asset with EU export restrictions, compliance risk, and a 70 to 80% operational ceiling. A lower price might be achievable if the EU sanction is lifted as a condition of the Rosneft exit. No mechanism exists to coordinate this outcome.

Microsoft: Restored services after eight days, said nothing about future compliance decisions, and continues operating in a $27 billion Indian cloud market where it and AWS hold the dominant positions. The Finance Ministry’s blocking statute proposal, when enacted, will require Microsoft to formally choose between complying with Indian law and complying with its EU compliance interpretation. That choice has not yet been forced.

💼Insights:

The Nayara case is the clearest available demonstration that foreign ownership of Indian strategic infrastructure carries a regulatory risk not captured in standard political risk insurance frameworks.

Political risk insurance covers expropriation, currency inconvertibility, and political violence. It does not cover the scenario in which a foreign government sanctions the infrastructure you own in a third country, a US technology company interprets that sanction extraterritorially, and your refinery is partially paralyzed not by any Indian government action but by a cloud service suspension in Washington state.

The asset is not expropriated. It is operationally degraded by the compliance behavior of its technology vendors, acting on their interpretation of a sanction that has no legal authority in the jurisdiction where the asset operates.

This risk is not priced into the investment models of any entity that evaluated Indian energy infrastructure before July 2025. It is the risk that needs to be priced into every evaluation after it.

The eight-day period between Microsoft’s suspension and restoration is the clearest available case study in what extraterritorial sanctions compliance by a technology company costs in legal liability, in relationship damage, in regulatory response, and in the precedent it sets for future compliance decisions by every technology company operating in the same jurisdiction.

Microsoft’s restoration of services was not a policy change. It was a tactical retreat under judicial pressure. The company has not stated what it will do when the next EU designation affects an Indian customer. The Indian government has not enacted the blocking statute that would make that decision costly. The window between the judicial retreat and the legislative response is the window in which every technology company operating in India is deciding, quietly, what its compliance policy will be when the next designation arrives.

🎯 The pattern

Three cases examined. One mechanism in all of them.

BP in Russia: Aligned investment from 1997, generating returns through 2021, $25 billion write-down in 48 hours in 2022, three years of negotiation that produced no clean exit. The asset became a hostage when the alignment broke.

Aramco’s nationalization: US companies held the asset, Saudi Arabia held the sovereignty. When Saudi Arabia decided to reclaim the asset, the terms of the transition were set by the sovereign. The transition was structured because both parties had something to lose from an unstructured one.

Shell in Nigeria: Environmental liability and absence of qualified buyers produced a 65-year hold in an asset Shell could not operate cleanly. Resolution came only when a consortium buyer was assembled and regulatory requirements were met over two years.

Nayara 2026: Russian company holds the asset. India holds the sovereignty but doesn’t want the asset. The EU holds the sanction but doesn’t hold the jurisdiction. The US technology company holds the off-switch but didn’t need to flip it. No party controls enough variables to force the resolution unilaterally.

The pattern is not that foreign investment in strategic energy infrastructure is always a trap. It is that foreign investment in strategic energy infrastructure becomes a trap precisely when it is no longer needed when the geopolitical relationship that made the investment attractive has changed, when the host country’s strategic interests have realigned, and when the exit is blocked by the valuation disagreement between what the investor paid and what the asset is now worth under the new political environment.

The Nayara problem will be resolved when one of three things happens: Rosneft accepts a price that reflects the post-sanction asset value. The EU lifts the sanction as part of a larger Russia-Ukraine diplomatic resolution. Or India’s Finance Ministry enacts the blocking statute and forces every technology company operating in India to choose Indian law over extraterritorial compliance changing the digital sovereignty calculus for every multinational operating on Indian soil.

The machinery for all three resolutions exists. None of them is activated. The refinery runs at 70 to 80% capacity. The cloud services are restored for now. The Finance Ministry proposal sits in draft. And 8% of India’s crude throughput continues to be processed by a facility whose ownership, feedstock, regulatory status, and digital infrastructure are all simultaneously contested.

📌 Takeaways

“Microsoft suspended cloud access to India’s second-largest private refinery for eight days based on its own interpretation of a European sanction, with no legal authority under Indian or US law to do so. The refinery is in Gujarat. The off-switch was in Washington state. That is what energy sovereignty means in 2026: not the right to produce your own oil, but the right to run your own refinery without a foreign cloud company deciding to shut it down.”

“Rosneft paid $12.9 billion for Nayara in 2017. It is offering to sell for $17 billion. No buyer will pay it. The EU sanction impairs the asset. The compliance risk deters traders. The Hormuz war made the feedstock politically toxic. The price Rosneft wants reflects the asset before the sanctions. The price any buyer will offer reflects the asset after them. That gap between what was paid and what can be recovered is what a geopolitical trap costs when you are the one inside it.”

“India’s Finance Ministry is proposing a blocking statute modeled on a 1996 EU law that prevents Indian-registered companies from complying with foreign sanctions on Indian soil. The EU created the blocking statute to protect European companies from US sanctions. India is now considering copying it to protect Indian companies from EU sanctions enforced by US technology companies. The instrument of protection has circled back to the continent it was designed to protect against.”

📚 References:

Data Center Dynamics, “Microsoft cuts off cloud services to Rosneft-backed Nayara Energy,” updated March 31, 2026 - 70-80% capacity figure, Microsoft suspension, Nayara statement

WorldECR, “EU-sanctioned Indian refiner sues Microsoft over service suspension,” July 31, 2025 Nayara Delhi High Court filing, Microsoft extraterritorial compliance analysis

BizzBuzz, “Microsoft reinstates services to sanctioned Indian refiner,” July 30, 2025 service restoration timeline, eight days, pre-hearing capitulation

The Daily Jagran, “Sanctioned Nayara Energy sues Microsoft after IT services suspension, turns to Rediff for support,” July 30, 2025 - Rediff.com transition, Teams and Outlook suspension

KBS Sidhu Substack, “Microsoft-Nayara Energy Case: India’s Digital Sovereignty Wake-Up Call,” August 3, 2025 - Delhi High Court July 28 filing, July 30 hearing, Microsoft restoration

Inc42, “Microsoft-Nayara Energy Case Exposes India Inc’s Cloud Risk,” August 6, 2025 - $27 billion India cloud market, Microsoft and AWS dominance, sovereign cloud debate

India Daily Mail, “Govt Considers Law Shielding Firms from Foreign Sanctions,” April 2026 Finance Ministry blocking statute proposal, EU 1996 statute model, sovereign cloud alternative

Rosneft official statement, “Statement of Rosneft Oil Company Regarding Illegal EU Sanctions on Nayara Energy Refinery,” July 2025 Rosneft’s characterization of sanction, less-than-50% framing, Indian legal entity argument

Business Standard, “Unable to repatriate earnings, Rosneft looks for an exit from Nayara Energy,” March 21, 2025 exit decision, $20 billion initial valuation, potential buyers

Business Standard, “Russia’s Rosneft in early talks with Reliance to sell stake in Indian unit,” June 29, 2025 Reliance preliminary talks, Adani decline, ONGC-IOC low valuation, $17 billion revised ask

BusinessToday, “Rosneft in early talks with Reliance for stake sale in Nayara Energy,” June 29, 2025 -Saudi Aramco interest, Trafigura exit likely if deal closes, valuation per petrol pump analysis

Business Standard, “EU imposes sanctions on Rosneft’s India refinery, lowers oil price cap,” July 18, 2025 -18th sanctions package, EU designation details

OilPrice.com, “Microsoft Reinstates Services to Sanctioned Indian Refiner,” July 31, 2025 shadow fleet context, EU 18th package scope

Daniel Yergin, The New Map: Energy, Climate, and the Clash of Nations (Penguin Press, 2021) historical FDI in energy infrastructure and geopolitical realignment

BP Annual Report 2022 TNK-BP write-down, Rosneft stake exit, $25 billion impairment

Platform for Peace and Humanity, “Shell’s Decades of Devastation: Niger Delta Oil Spills and the Long Road to Justice,” 2023 - SPDC history, 2023 sale timeline

If this changed how you see sovereignty subscribe. If it didn’t tell me why. I read everything.